Last year, as many as 1 in 3 sellers took their home off the market because it wasn’t selling. If this happened to you too, you don’t need to be embarrassed. What you need are answers. And a local real estate agent can help with that by seeing if it was priced too high, needs some repairs, or didn’t get the right exposure. If you still want to move, let’s connect to come up with a new strategy. Together, we can get your house sold.

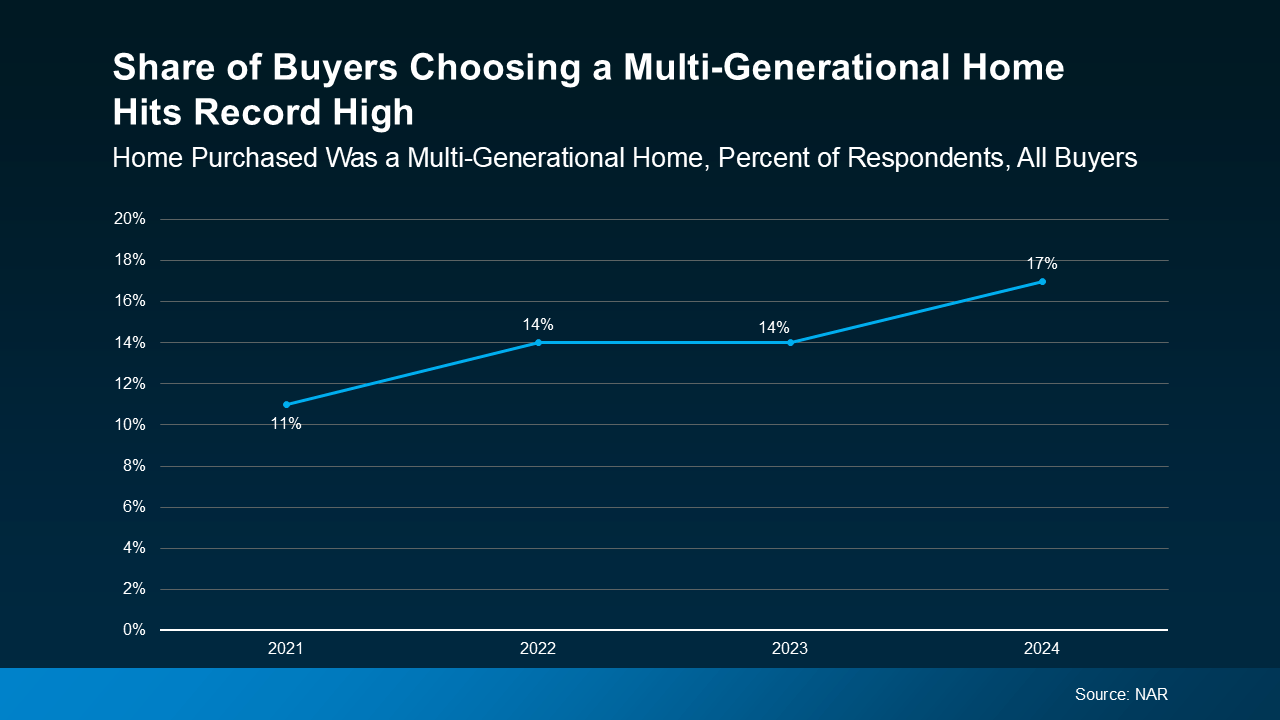

Today, 17% of homebuyers are choosing multi-generational homes — that’s when you buy a house with your parents, adult children, or even distant relatives. What makes that noteworthy is that 17% is actually the highest level ever recorded by the National Association of Realtors (NAR). But what’s driving the recent rise in multi-generational living?

Top Benefits of Choosing a Multi-Generational Home

In the past, homebuyers often opted for multi-generational homes to make it easier to care for their parents. And while that’s still a key reason, it’s not the only one. Right now, there’s another powerful motivator: affordability.

According to the latest data from NAR, cost savings are the main reason more people are choosing to live with family today.

The rising cost of homeownership is making it harder for many people to afford a home on their own. This has led to more families pooling their resources to make buying a home possible.

By combining incomes and sharing expenses like the mortgage, utility bills, and more, multi-generational living offers a way to overcome financial challenges that might otherwise put homeownership out of reach. As Rick Sharga, Founder and CEO at CJ Patrick Company, explains:

“There are a few ways to improve affordability, at least marginally. . . purchase a property with a family member — there are a growing number of multi-generational households across the country today, and affordability is one of the reasons for this.”

You may even find it helps you afford a bigger home than you would have been able to on your own. So, if you need more room, but can’t afford it with today’s rates and prices, this could be an option to still get the space you need.

On top of the financial benefits, it could also bring your family closer together and strengthen your bonds by getting more quality time together.

Bottom Line

If you’re considering a move, buying a multi-generational home might be worth exploring – especially if your budget is stretched too thin on your own.

Let’s discuss your needs and find a home that fits your family’s unique situation.

Wondering what to expect when you buy or sell a home this year? Here’s what the experts say lies ahead. Mortgage rates are projected to come down slightly. Home prices are forecast to rise in most areas. And, there will be more homes available for sale. Want to know more about what this could mean for your plans this year? Let’s connect to discuss your 2025 goals.

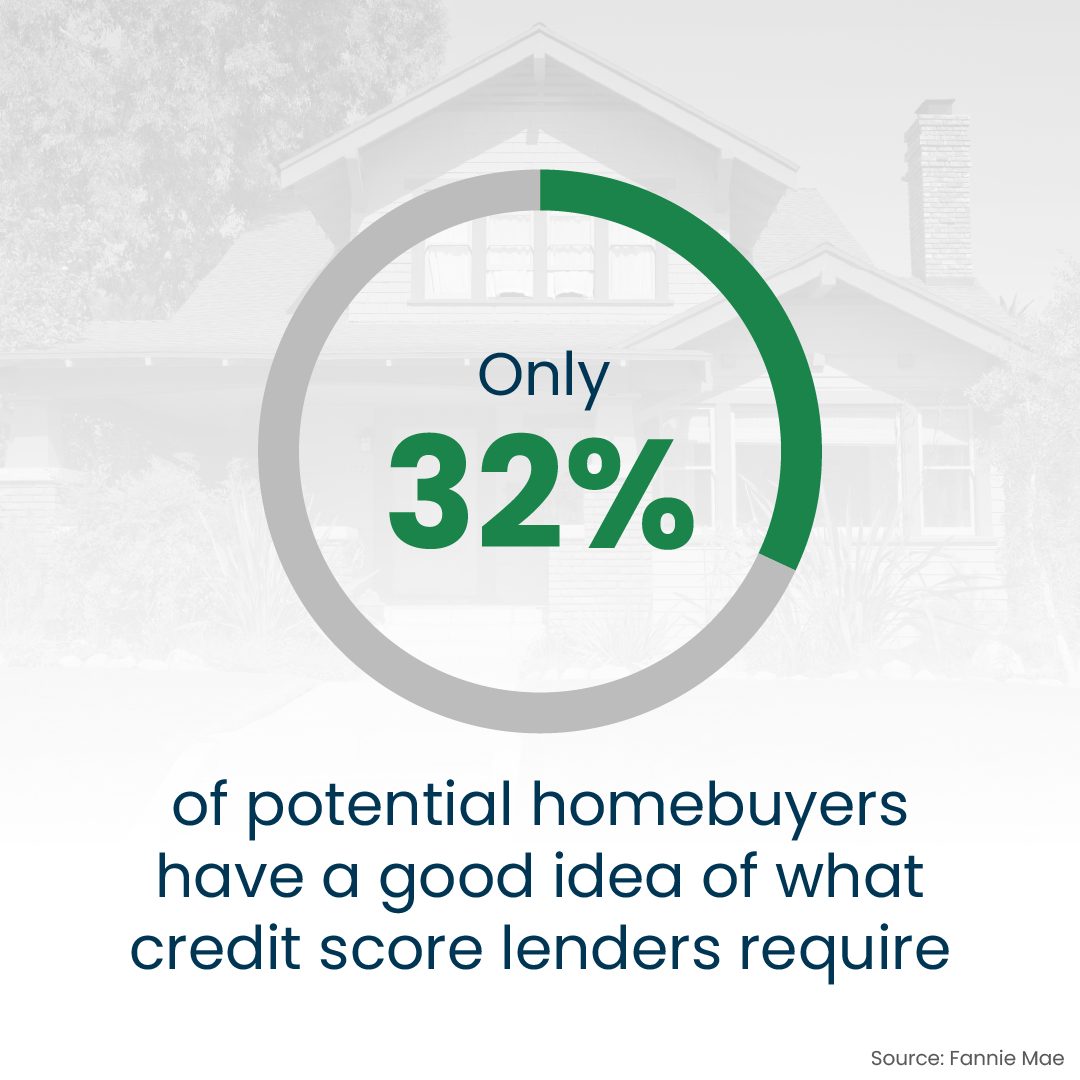

Your credit score is an important factor when you apply for a mortgage. But most people don’t know what lenders actually require. Despite what you may have heard, you don’t need a perfect score to get a home loan. There are loans out there for buyers with a range of credit scores. The best way to know what you’d qualify for? Talk with a local lender who can walk you through your options.

Are you hesitant to sell your house because you’re worried no one’s buying with rates and prices where they are right now? Here’s some perspective that can help.

The market actually isn’t at a standstill. While there weren’t as many sales last year as there’d be in a normal market, roughly 4.15 million homes still sold (not including new construction), according to the National Association of Realtors (NAR). And the expectation is that number will rise in 2025. That means more people will likely move this year, and they need homes to buy. Homes like yours.

But even if we only match last year’s sales pace, here’s what that looks like.

Every Minute Homes Are Selling – Literally

4.15 million homes ÷ 365 days in a year = 11,370 homes sell each day

11,370 homes ÷ 24 hours in a day = 474 homes sell per hour

474 homes ÷ 60 minutes = roughly 8 homes sell every minute

Think about that. Just in the time it took you to read this, 8 homes sold.

If you’ve been holding off on selling your house because you think buyers aren’t out there, let this reassure you – there are still buyers looking to buy.

Every day, thousands of people need to buy homes. So, while higher home prices and mortgage rates have slowed the market down and forced some buyers onto the sidelines, that doesn’t mean the market isn’t active. Many buyers are still eager to make a move because life doesn’t wait for perfect market conditions.

With the right agent by your side, you can get your house in front of those buyers while other hesitant homeowners are still putting their plans on pause because they’re worried buyer demand has disappeared. Let’s get your house sold.

Bottom Line

On average, over 11,000 homes sell every day, and yours could be one of them. In the time it took you to read this, another 8 homes sold.

When you’re ready to take the next step, let’s connect so you have an agent to create that perfect strategy.

Trying to decide whether it makes more sense to buy a home now or wait? There’s a lot to consider, from what’s happening in the market to your changing needs. But generally speaking, aiming to time the market isn’t a good strategy – there are too many factors at play for that to even be possible.

That’s why experts usually say time in the market is better than timing the market.

In other words, if you want to buy a home and you’re able to make the numbers work, doing it sooner rather than later is usually worth it. Bankrate explains why:

“No matter which way the real estate market is leaning, though, buying now means you can start building equity immediately.”

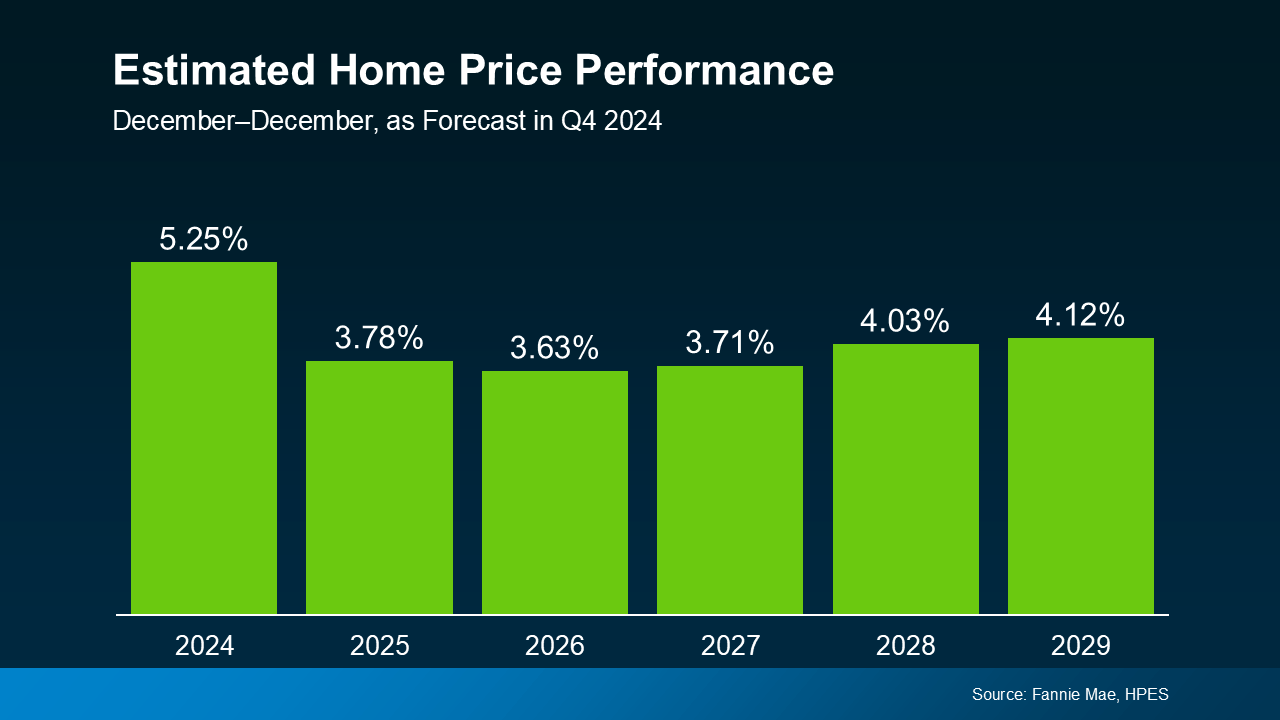

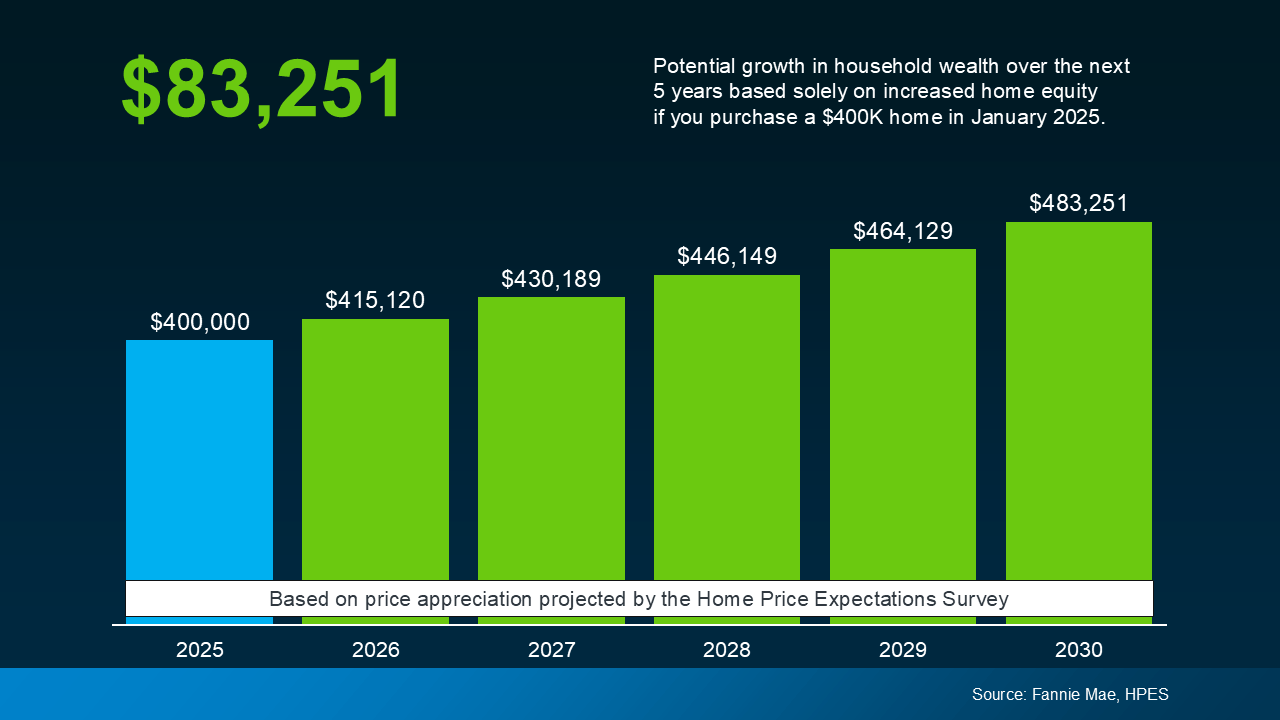

Here’s some data to break this down so you can really see the benefit of buying now versus later – if you’re able to. Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2029 – just at a slower, more normal pace than they did over the past few years (see the graph below):

But what does that really mean for you? To give these numbers context, the graph below uses a typical home value to show how it could appreciate over the next few years using those HPES projections (see graph below). This is what you could start to earn in equity if you buy a home in early 2025.

In this example, let’s say you go ahead and buy a $400,000 home this January. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. If you keep on renting, you’re losing out on this equity gain.

And while today’s market has its fair share of challenges, this is why buying is going to be worth it in the long run. If you want to buy a home, don’t give up. There are creative ways we can make your purchase possible. From looking at more affordable areas, to considering condos or townhomes, or even checking out down payment assistance programs, there are options to help you make it happen.

So sure, you could wait. But if you’re just waiting it out to perfectly time the market, this is what you’re missing out on. And that decision is up to you.

Bottom Line

If you’re torn between buying now or waiting, don’t forget that it’s time in the market, not timing the market that truly matters. Let’s connect if you want to talk about what you need to do to get the process started today.

You may have heard that staging your home properly can make a big difference when you sell your house, but what exactly is home staging, and is it really worth your time and effort?

Here are a few quick FAQs that can help you decide how much you should prioritize staging as you prep for your move.

What Is Home Staging?

Staging is the process of arranging and decorating your house to highlight its best features and make it as appealing as possible to potential buyers. It can range from simple touch-ups to more extensive setups, depending on your needs and budget.

How Does It Help Me Sell My House?

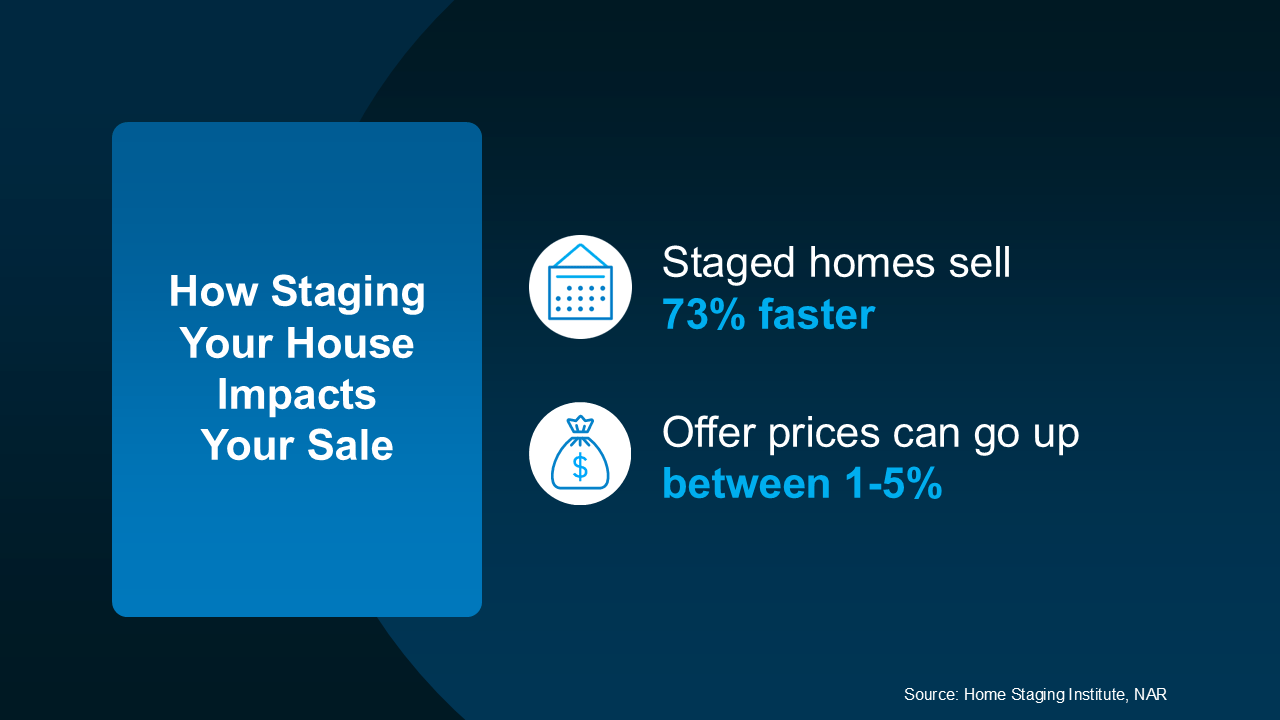

Studies show good staging does have an impact on your sale. Staging your house well can help you attract more attention from buyers, which ultimately helps it sell faster and maybe for a higher price than an unstaged home (see visual):

What Are My Staging Options?

Now that you see the value, let’s think through your options. The most common is leaning on your agent for their expert advice. They know what buyers like because they’re in showings all the time and hear that feedback first-hand. That expertise is crucial to getting your house market-ready. Basic staging with an agent usually means they give you insight into how you should:

Declutter and depersonalize by removing photos and personal items

Arrange your furniture to improve the room’s flow and make it feel bigger

Add plants, move art, or re-arrange other accessories

Full-service staging is another option if your house needs more hands-on attention. This is when you hire a staging professional or staging company to come in, make recommendations, and do the work for you. Going this route is more involved and that makes it more costly too. That’s because it can include renting furniture and decor to more fully transform a space.

How Do I Know Which One To Pick?

Not sure which one you need? You don’t have to figure that out on your own. Your real estate agent will help determine what level of staging will make the most impact on your house and market.

They can help you decide if professional staging is worth the investment, or if you can knock it out with their advice alone. And just so you know, here are some of the factors an agent will look at to figure that out:

Market Conditions: If the market is slower, going all in on staging can make your home look move-in ready and attractive to buyers who may otherwise be hesitant. If your local market is very active and homes are selling fast, you may be able to get by with doing less.

Your Home’s Condition: If your home is vacant or has a unique layout, using a professional stager who can bring in the right furniture and accessories may help buyers truly visualize its full potential.

Your Budget: Talk to your agent to get an idea of staging costs in your area, as it can be the difference between your house selling and sitting.But if your budget is tight or your home only needs minor updates, your real estate agent can help you think outside of the box by suggesting simple DIY staging tips to help your home look its best.

Bottom Line

Staging your house properly can make it much more attractive to buyers, but it’s not a one-size-fits-all solution, and every home shines differently. Let’s connect to talk through what your home really needs to stand out and sell for top dollar.

There’s no doubt that owning a home comes with significant financial benefits. And this time of year is a great time to reflect on the other reasons why owning a home is so meaningful.

A house is more than four walls and a roof – it’s a place where memories are made, connections are built, and life happens.

From the sense of accomplishment that comes with owning your own home to the joy of creating a space that’s uniquely yours, the emotional connections we have to our homes can be just as important as the financial ones.

Here are some of the things that turn a house into a happy home.

1. It’s an Accomplishment You Can Be Proud Of

Buying a home is a significant milestone, whether it’s your first or your fifth. You’ve worked hard to make it happen and achieving this goal is a reason to celebrate. There’s nothing quite like stepping through the door of a home that’s yours and knowing you’ve accomplished something truly special.

2. It’s a Place You Can Call Your Own

Compared to renting, owning a home can give you a much greater sense of security and privacy. It’s your own place – not your landlord’s – and that just feels different. No one else has the keys but you and that gives you your own personal safe place to retreat to at the end of a long day.

3. It’s a Space That’s Yours To Customize

Owning a home means you have the freedom to personalize it however you like. While there can be HOA guidelines you may have to follow depending on where you buy, you can still make it a reflection of your style and create a space that feels just right for you. As Freddie Macexplains:

“As the homeowner, you have the freedom to adopt a pet, paint the walls any color you choose, renovate your kitchen, and more. You can customize your own space without approval from landlords.”

4. It’s a Foundation for Building a Sense of Community

Homeownership often means putting down roots in a neighborhood and becoming a part of the local community. According to groups like Habitat for Humanity, owning a home increases your interest in getting involved with your neighbors and local organizations. Whether it’s through joining a neighborhood group, volunteering, or simply getting to know the people next door, a home is a great foundation for building meaningful connections.

Bottom Line

Owning a home is about so much more than financial benefits – it’s about the pride, well-being, and sense of belonging it can bring. When you’re ready to take the next step toward buying a home, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Top Benefits of Choosing a Multi-Generational Home

Top Benefits of Choosing a Multi-Generational Home

What Are My Staging Options?

What Are My Staging Options?