Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Uncategorized •

August 21, 2023

Why Median Homes Sales Price Is So Confusing Right Now!

The National Association of Realtors (NAR) is set to release its most recent Existing Home Sales (EHS) report tomorrow. This monthly release provides information on the volume of sales and price trends for homes that have previously been owned. In the upcoming release, it’ll likely say home prices are down. This may seem a bit confusing, especially if you’ve been following along and reading the blogs saying home prices have hit the bottom and have since rebounded.

So, why would this say home prices are falling when so many other price reports say they’re going back up? It all depends on the methodology of each one. NAR reports on the median home sales price, while some other sources use repeat sales prices. Here’s how those approaches differ.

The Center for Real Estate Studies at Wichita State University explains median sales prices like this:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less . . . For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

Investopedia helps define what a repeat sales approach means:

“Repeat-sales methods calculate changes in home prices based on sales of the same property, thereby avoiding the problem of trying to account for price differences in homes with varying characteristics.”

The Challenge with the Median Home Sales Price Today

As the quotes above say, the approaches can tell different stories. That’s why median home sales price data (like EHS) may say prices are down, even though the vast majority of the repeat sales reports show prices are appreciating again.

Bill McBride, Author of the Calculated Risk blog, sums the difference up like this:

“Median prices are distorted by the mix and repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices.”

To drive this point home, here’s a simple explanation of median value (see visual below). Let’s say you have three coins in your pocket, and you decide to line them up according to their value from low to high. If you have one nickel and two dimes, the median value (the middle one) is 10 cents. If you have two nickels and one dime, the median value is now five cents.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change.

That’s why using the median home sales price as a gauge of what’s happening with home values may be confusing right now. Most buyers look at home prices as a starting point to determine if they match their budgets. But most people buy homes based on the monthly mortgage payment they can afford, not just the price of the house. When mortgage rates are higher, you may have to buy a less expensive home to keep your monthly housing expense affordable.

That’s why a greater number of ‘less-expensive’ houses are selling right now – and that’s causing the median home sales price to decline. But that doesn’t mean any single house lost value.

When you see the stories in the media that prices are falling later this week, remember the coins. Just because the median home sales price changes, it doesn’t mean home prices are falling. What it means is the mix of homes being sold is being impacted by affordability and current mortgage rates.

Bottom Line

For a more in-depth understanding of home price trends and reports, let’s connect.

Market Information •

August 19, 2023

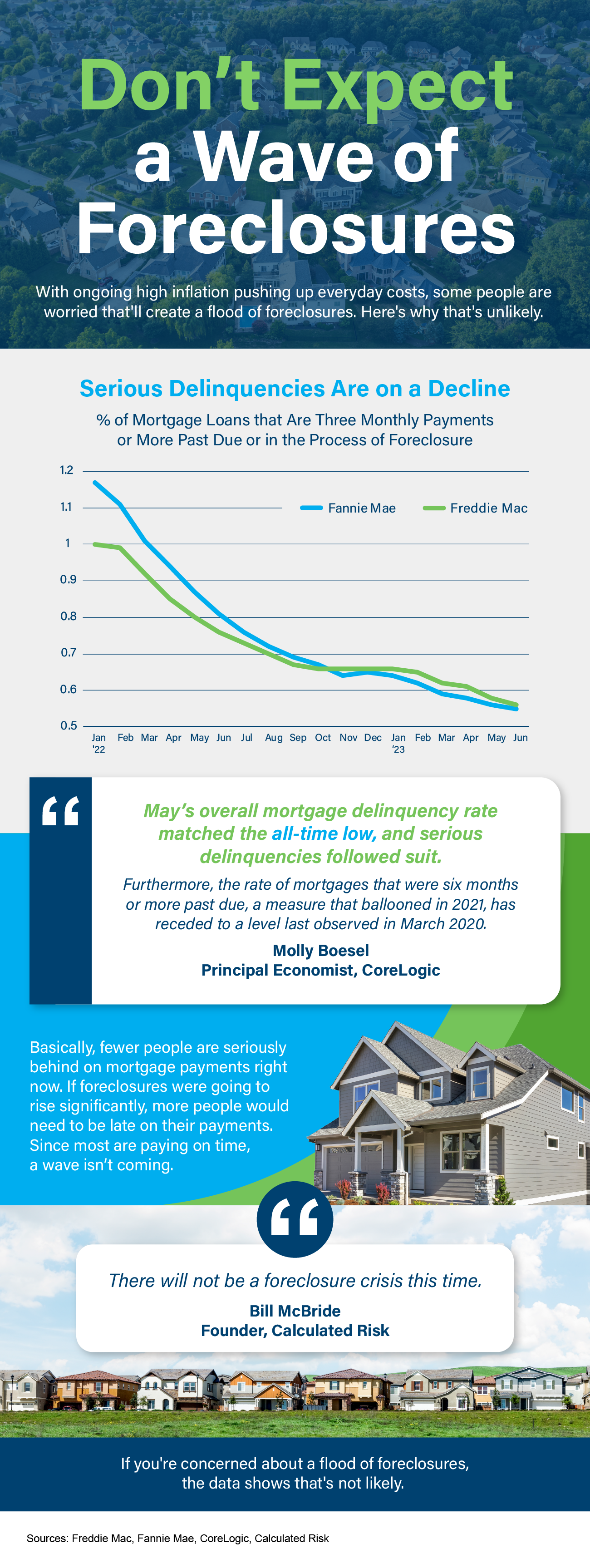

Don’t Expect a Wave of Foreclosures- Inforgraphic

Some Highlights

- With ongoing high inflation pushing up everyday costs, some people are worried that’ll create a flood of foreclosures. Here’s why that’s unlikely.

- Fewer people are seriously behind on mortgage payments right now. If foreclosures were going to rise a lot, more people would need to be late on their payments.

- Since most are paying on time, a wave isn’t coming. If you’re concerned about a flood of foreclosures, the data shows that’s not likely.

Uncategorized •

August 17, 2023

People Want Less Expensive Homes- And Builders Are Responding

In today’s housing market, there are two main affordability challenges impacting buyers: mortgage rates that are higher than they’ve been the past couple of years, and rising home prices caused by low inventory. To overcome those challenges, many people are working with their agents to find less expensive homes. And with newly built homes making up a historically large percentage of the total available inventory today, that search often includes brand new homes.

People Are Spending Less on Newly Built Homes

The graph below uses the latest information from the Census to show, in June, more of the newly built home sales in this country were in lower price ranges than in 2022: Last year, only 58% of newly built home sales were less than $500,000. This June, that number was up to 65%. This means more people are buying less expensive newly built homes right now while affordability remains a challenge.

Last year, only 58% of newly built home sales were less than $500,000. This June, that number was up to 65%. This means more people are buying less expensive newly built homes right now while affordability remains a challenge.

Builders Are Offering Lower-Cost Options

Builders have picked up on this trend and are reacting accordingly. George Ratiu, Chief Economist at Keeping Current Matters, explains:

“Builders are also responding to this shift by bringing slightly smaller homes to market in an effort to meet lower price points . . .”

New data from the Census further confirms this pattern – it shows the median sales price of newly built homes has dipped down in recent months (see graph below): And as Mikaela Arroyo, Director of the New Home Trends Institute at John Burns Real Estate Consulting, says, the builders who are most responsive to this trend are forming pathways to homeownership:

And as Mikaela Arroyo, Director of the New Home Trends Institute at John Burns Real Estate Consulting, says, the builders who are most responsive to this trend are forming pathways to homeownership:

“. . . it is creating opportunities for people to be able to afford an entry-level home in an area. . . . if you get that size down, that automatically will make it a more affordable home. The [builders] that are decreasing [size] the most are probably the ones that try to build more of an affordable product.”

How an Agent Can Help

Builders producing smaller, less expensive newly built homes give you more affordable options at a time when that’s really needed. If you’re hoping to buy a home soon, partner with a local real estate agent to find out what’s available in your area. An agent can help you look at newly built homes or ones under construction nearby.

Bottom Line

If you’re having a hard time finding a home you like in your budget, let’s connect. You need a real estate professional who knows all about the latest inventory in our area, including homes still under construction or just built. That way you have an expert on your side who can provide information on builder reputations, builder contracts and negotiations, and more to help you with the homebuying process.

Uncategorized •

August 15, 2023

Equity is a Game Changer for Home Owners Looking to Sell!

August 15, 2023

If you’re a homeowner, you might be torn on whether or not to sell your house right now. Maybe that’s because you don’t want to take on a higher mortgage rate on your next home. If that’s your biggest hurdle, understanding your equity may be exactly what you need to help you feel more comfortable making your move.

What Equity Is and How It Works

Equity is the current value of your home minus what you owe on the loan. And recently, that equity has been growing far faster than you may expect.

Over the last few years, home prices rose dramatically, and that gave your equity a big boost very quickly. While the market has started to normalize, there’s still an imbalance between the number of homes available for sale and the number of buyers looking to make a purchase. And it’s because homes are in such high demand that prices are back on the rise today. Rob Barber, CEO of ATTOM, a property data provider, explains:

“Equity levels were high even during the recent downturn, and now they are going back up and better than ever.”

How Equity Benefits You in Today’s Market

With today’s affordability challenges, that equity can be a game changer when you move. Here’s why. Based on data from ATTOM and the Census, nearly two-thirds (68.7%) of homeowners have either paid off their mortgages or have at least 50% equity (see chart below):

That means roughly 70% have a tremendous amount of equity right now.

Once you sell your house, you can use your equity to help with your next purchase. It could be some (if not all) of what you’ll need for your next down payment. It may even be enough to allow you to put a considerably larger down payment on your next home, so you don’t have to finance quite as much. And, if you’ve been in your current house for years, you may have even built up enough equity to pay in all cash. If that’s true for you, you’d be able to avoid borrowing altogether, so you wouldn’t have to worry about today’s mortgage rates.

How To Find Out How Much Equity You Have

The best way to learn how much you have is to reach out to a trusted real estate agent for a Professional Equity Assessment Report (PEAR).

Bottom Line

If you’re planning to make a move, the equity you’ve gained can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

Market Information •

August 8, 2023

There is only HALF the inventory of a normal housing market!

Wondering if it still makes sense to sell your house right now? The short answer is, yes. Especially if you consider how few homes there are for sale today.

You may have heard inventory is low right now, but you may not fully realize just how low or why that’s a perk when you go to sell your house. This graph from Calculated Risk can help put that into perspective:

As the graph shows, while housing inventory did grow slightly week-over-week (shown in the blue bar), overall supply is still low (shown in the red bars). Compared to the same week last year, supply is down roughly 10% – and it was already considered low at that time. But, if you look further back, you’ll see inventory is down even more significantly.

As the graph shows, while housing inventory did grow slightly week-over-week (shown in the blue bar), overall supply is still low (shown in the red bars). Compared to the same week last year, supply is down roughly 10% – and it was already considered low at that time. But, if you look further back, you’ll see inventory is down even more significantly.

To gauge just how far off from normal today’s inventory is, let’s compare right now to 2019 (the last normal year in the market). When you compare the same week this year with the matching week in 2019, supply is about 50% lower. That means there are half the homes for sale now than there’d usually be.

The key takeaway? We’re still nowhere near what’s considered a balanced market. There’s plenty of demand for your house because there just aren’t enough homes to go around. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“There are simply not enough homes for sale. The market can easily absorb a doubling of inventory.”

So, if you want to list your house, know that there’s only about half the inventory there’d usually be in a more normal year. That means your house will be in the spotlight if you sell now and you may see multiple offers and a fast home sale.

Bottom Line

With the number of homes for sale roughly half of what there’d usually be in a more normal year, you can rest assured there’s demand for your house. If you want to sell, let’s connect now so your house can shine above the rest while inventory is so low.

Home Owners • Market Information •

August 7, 2023

4 Ways You Can Use Your Equity

Four Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years. Equity builds over time as home values grow and as you pay down your home loan. And, since home prices skyrocketed during the ‘unicorn’ years, you’ve likely gained more than you think.

According to the latest Equity Insights Report from CoreLogic, the average homeowner has more than $274,000 in equity right now. That much equity can help you achieve certain goals. In a recent article, Bankrate elaborates:

“While the pandemic created serious challenges, the silver lining for anyone who owned a home was the sizable equity gain. Understanding how home equity works, and how to leverage it, is important for any homeowner.”

Here are a few examples of how you can put your home equity to work for you.

1. Buy a Home That Fits Your Needs

If your current space no longer meets your needs, it might be time to think about moving to a bigger home. And if you’ve got too much space, downsizing to a smaller home could be just right. Either way, you can put your equity toward a down payment on a home that fits your changing lifestyle. A real estate agent can help you figure out how much equity you’ve got and how to use it when buying your next home.

2. Reinvest in Your Current Home

Renovations are a great option if you want to change your living space, but you aren’t yet ready to make a move. Home improvement projects give you the freedom to tailor your home to match your needs and personal style. But it’s important to consider the long-term benefits certain upgrades can bring to your home’s value. Lean on a real estate professional for the best advice on which improvement projects to prioritize in order to get the greatest return on your investment when you sell later on.

3. Pursue Personal Ambitions

Home equity can also serve as a catalyst for realizing your life-long dreams. That could mean investing in a new business venture, retirement, or funding an education. While you shouldn’t use your equity for unnecessary spending, using it responsibly for something meaningful and impactful can really make a difference in your life.

4. Understand Your Options to Avoid Foreclosure

Today the number of foreclosure filings remains below the norm, so there’s no need to fear a wave of foreclosed homes flooding the market. But unfortunately, there are still some homeowners who experience the foreclosure process each year. If you’re facing financial difficulties, having a clear understanding of your options and how your equity can help is crucial. Equity can act as a financial cushion that can be used in times of unexpected challenges or unforeseen circumstances that may disrupt your ability to make mortgage payments on time.

In an article, Freddie Mac explains it this way:

“If exiting your home is the best option for you, selling with equity may be a good option. When selling with equity, you are using the proceeds from selling your home at a higher price than the amount you owe on your mortgage to pay off your remaining mortgage debt.”

Bottom Line

Your equity can be a game changer in reinvesting in your needs, pursuing your goals, and even helping you avoid foreclosure during difficult times. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

Market Information •

August 3, 2023

How Inflation Affects Interest Rates

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here’s what you need to know.

The Fed is trying hard to reduce inflation. And even though there’s been 12 straight months where inflation has cooled (see graph below), the most recent data shows it’s still higher than the Fed’s target of 2%:

While you may have been hoping the Fed would stop their hikes since they’re making progress on their goal of bringing down inflation, they don’t want to stop too soon, and risk inflation climbing back up as a result. Because of this, the Fed decided to increase the Federal Funds Rate again last week. As Jerome Powell, Chairman of the Fed, says:

“We remain committed to bringing inflation back to our 2 percent goal and to keeping longer-term inflation expectations well anchored.”

Greg McBride, Senior VP, and Chief Financial Analyst at Bankrate, explains how high inflation and a strong economy play into the Fed’s recent decision:

“Inflation remains stubbornly high. The economy has been remarkably resilient, the labor market is still robust, but that may be contributing to the stubbornly high inflation. So, Fed has to pump the brakes a bit more.”

Even though a Federal Fund Rate hike by the Fed doesn’t directly dictate what happens with mortgage rates, it does have an impact. As a recent article from Fortune says:

“The federal funds rate is an interest rate that banks charge other banks when they lend one another money . . . When inflation is running high, the Fed will increase rates to increase the cost of borrowing and slow down the economy. When it’s too low, they’ll lower rates to stimulate the economy and get things moving again.”

How All of This Affects You

In the simplest sense, when inflation is high, mortgage rates are also high. But, if the Fed succeeds in bringing down inflation, it could ultimately lead to lower mortgage rates, making it more affordable for you to buy a home.

This graph helps illustrate that point by showing that when inflation decreases, mortgage rates typically go down, too (see graph below):

As the data above shows, inflation (shown in the blue trend line) is slowly coming down and, based on historical trends, mortgage rates (shown in the green trend line) are likely to follow. McBride says this about the future of mortgage rates:

“With the backdrop of easing inflation pressures, we should see more consistent declines in mortgage rates as the year progresses, particularly if the economy and labor market slow noticeably.”

Bottom Line

What happens to mortgage rates depends on inflation. If inflation cools down, mortgage rates should go down too. Let’s talk so you can get expert advice on housing market changes and what they mean for you.